Discovering ways to save costs is constantly a concern, especially when it comes to required expenses such as car insurance. Auto insurance is not only a required duty in many places, but it also provides vital protection for you and your vehicle. Nevertheless, the costs can rapidly increase, resulting in many drivers looking for effective approaches to reduce their rates without compromising on coverage.

Luckily, there are several practical tips that can help you enhance your cost savings on vehicle insurance. From looking for better rates to taking advantage of discounts, making wise choices can lead to meaningful savings. In this resource, we will examine numerous methods you can employ to make sure you are not overpaying for your car insurance, allowing you to retain extra money in the pocket while still enjoying the peace of mind that comes with being well-insured. ## Comprehending Car Insurance Rates

Car insurance premiums are established by a variety of elements that can significantly impact the amount you spend. Insurance firms consider personal factors such as your years, male or female, and record. For example, younger individuals or those with a history of accidents or penalties may experience higher rates due to the assessed danger. Furthermore, the classification of car you use plays a significant role; high-performance cars frequently come with elevated insurance expenses.

An additional important factor in figuring your auto insurance costs is your geographic area. City regions with higher vehicle density often lead to greater rates, as the chance of accidents is higher. In comparison, countryside locations may have diminished rates due to less frequent accident frequency. Further local considerations, including theft rates and climate factors, can also influence your complete premium amount.

In conclusion, the coverage options you opt for and your selected deductible can significantly influence your insurance costs. Full coverage, which includes a larger range of benefits, will likely cost higher than a minimal policy. Additionally, opting for a greater deductible can reduce your periodic premium, but it also entails you'll pay greater out of pocket in the event of a claim. Grasping these considerations can help you arrive at informed choices about your car insurance to ultimately decrease your expenses.

Suggestions to Diminish Your Premium

One efficient way to lower your car insurance premium is to compare prices and evaluate quotes from different providers. Several insurance companies have varying rates and discounts, so it is wise to take the time to explore and find the most suitable deal. Utilize online comparison tools or consult with an insurance agent who can guide you through your possibilities and ensure you are obtaining the best coverage for your financial situation.

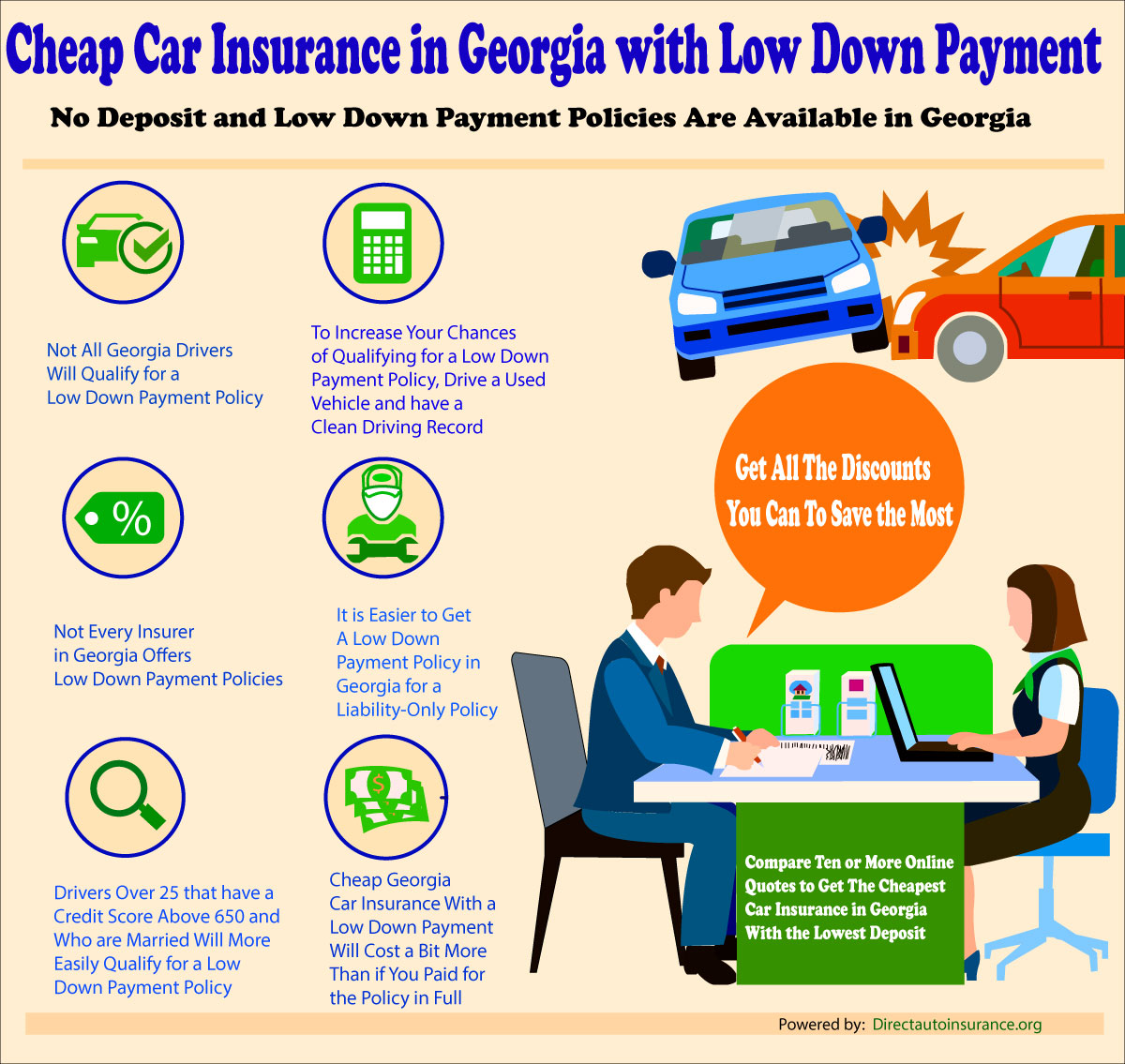

Another strategy is to raise your deductible. By choosing a larger deductible, you can significantly reduce your monthly premium. However, very cheap car insurance no deposit is important to ensure that you can easily afford the deductible in the event of a claim. Balancing a higher deductible with your budget can lead to savings while still providing you with sufficient protection.

In conclusion, consider taking advantage of available discounts. Many insurers offer discounts for different reasons, such as keeping a good driving record, bundling multiple policies, or being a participant of particular organizations. Interacting with your insurance provider to inquire about all possible discounts can help you maximize savings opportunities, making your auto insurance more manageable.

Assessing Insurance Options

When thinking about car insurance, it's crucial to review the coverage options offered to you. Begin by understanding the various types of coverage, including liability, collision, and comprehensive insurance. Liability coverage is typically required by law and covers you if you're at fault in an accident. Collision coverage helps pay for damage to your car after an accident, while comprehensive coverage safeguards against non-collision incidents such as theft or natural disasters.

Next, assess your personal needs and driving habits. If you have an older vehicle, you may want to think twice about whether collision and comprehensive coverage are essential, as the premiums may outweigh the car's value. Conversely, if you drive frequently or have a new car, higher coverage limits could provide security. Additionally, reflect on your financial situation and what you can afford in terms of deductibles and out-of-pocket expenses in the instance of a claim.

Finally, always compare quotes from multiple providers when reviewing coverage options. Rates can vary significantly between insurance companies, and discounts may be available based on factors including good driving records or bundling policies. Taking the time to shop around ensures you find the best policy that satisfies your coverage needs while assisting you cut on costs.